What happens when the children grow up and they are no longer dependent on their parents? Estate planning for mature families and retirees can bring up a number of issues including family dynamics and harmony. One of the most difficult conversations is around fair or equal distribution of assets. Before you begin putting a plan in place, we always encourage open conversation and a family meeting between the parents and children to provide context behind decisions and therefore it minimizes the surprises and provides an opportunity for children to express their concerns.

We’ve put together an infographic checklist that can help you get started on this. We know this can be a difficult conversation so we’re here to help and provide guidance.

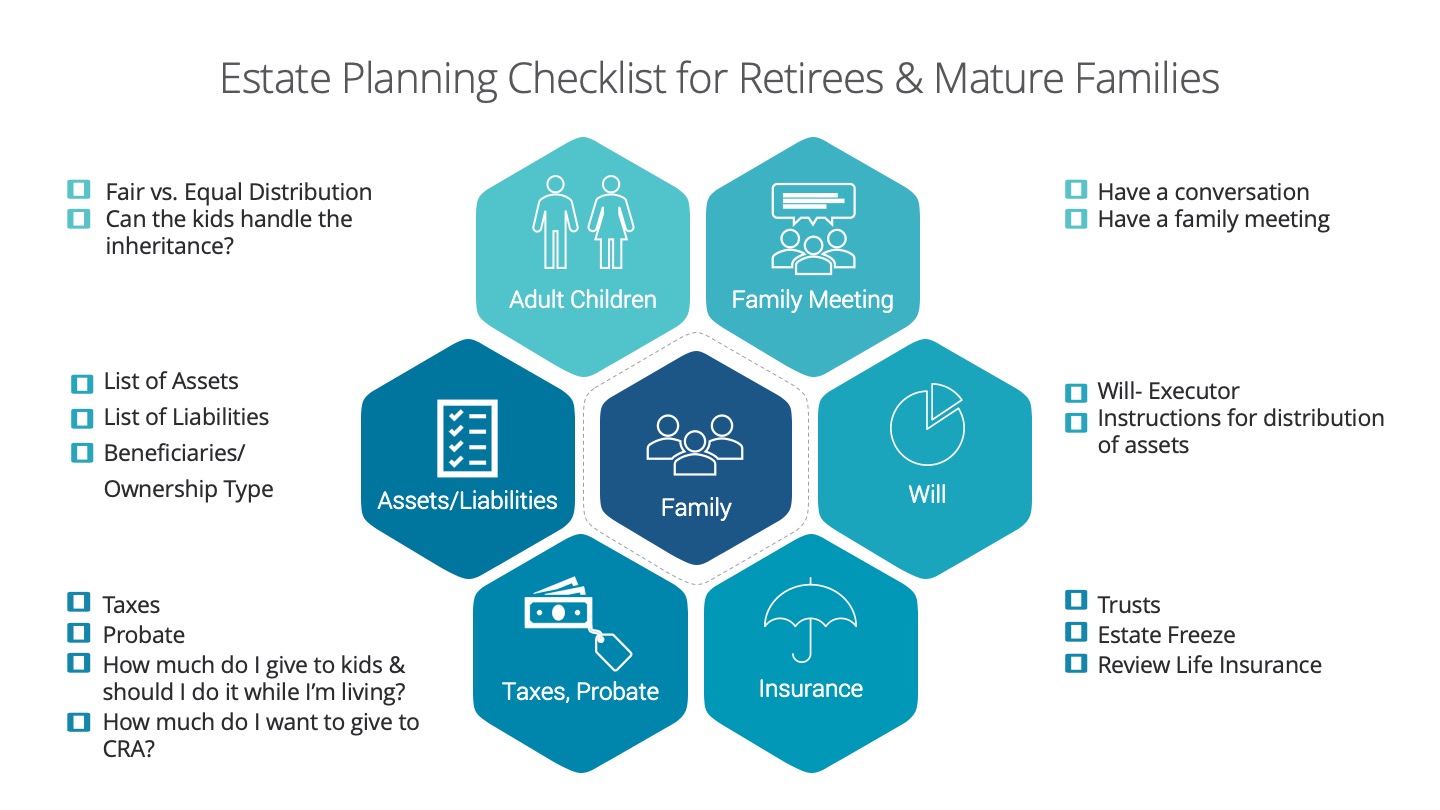

Adult Children

- Fair vs Equal (also known as Equitable vs Equal) – like what’s considered to be fair may not necessarily be equal. ex. Should the daughter that’s been working in the family business for 10 years receive the same shares as the son who hasn’t worked in the family business at all?

- Are the adult children responsible enough to handle the inheritance? Or would they spend it all?

Family Meeting

- Encourage open conversation with parents and kids so context can be provided behind the decisions, there are no surprises and allows the kids to express their interests and concerns.

- Facilitate a family meeting with both generations, this will help promote ongoing family unity after death and decrease the chances of resentment later.

Assets/Liabilities

- What are your assets? Create a detailed list of your assets such as:

- Home, Family Business Interest, Real Estate, Investments- Non registered, TFSA, RRSP, RDSP, RESP, Company Pension Plan, Insurance Policy, Property, Additional revenue sources, etc…

- What are your liabilities? Create a detailed list of your liabilities such as:

- Mortgage, Loans (personal, student, car), Line of Credit, Credit card, Other loans (payday, store credit card, utility etc.)

- Understand your assets-the ownership type (joint, tenants in common, sole etc.), list who are the beneficiaries are for your assets

- Understand your liabilities- are there any cosigners?

Make sure you have a will that:

- Assigns an executor

- Provide specific instructions for distribution of assets

- Always choose 2 qualified people for each position and communicate your intentions with them to ensure they’re up for the responsibility.

Taxes and Probate

- How much are probate and taxes? (Income tax earned from Jan 1 to date of death + Taxes on Non Registered Assets + Taxes on Registered Assets)

- Are there any outstanding debts to be paid?

- You’ve worked your whole life- how much of your hard earned money do you want to give to CRA?

- How much money do you want to to give to your kids while you’re living?

Consider the following:

- The use of trusts.

- The use of an estate freeze if you wish to gift while you’re living.

- Once you determine the amount of taxes, probate, debt, final expenses and gifts required, review your life insurance coverage to see if it meets your needs or if there’s a shortfall.

Execution: It’s good to go through this but you need to do this. Besides doing it yourself, here’s a list of the individuals that can help:

- Financial Planner/Advisor (CFP)

- Estate Planning Specialist

- Insurance Advisor

- Lawyer

- Accountant/Tax Specialist

- Chartered Life Underwriter (CLU)

- Certified Executor Advisor (CEA)

There are definitely unique situations in many families and things can get complicated so please use this when you feel it’s applicable.

Next steps…

- Contact us about helping you get your estate planning in order so you can gain peace of mind that your family is taken care of.